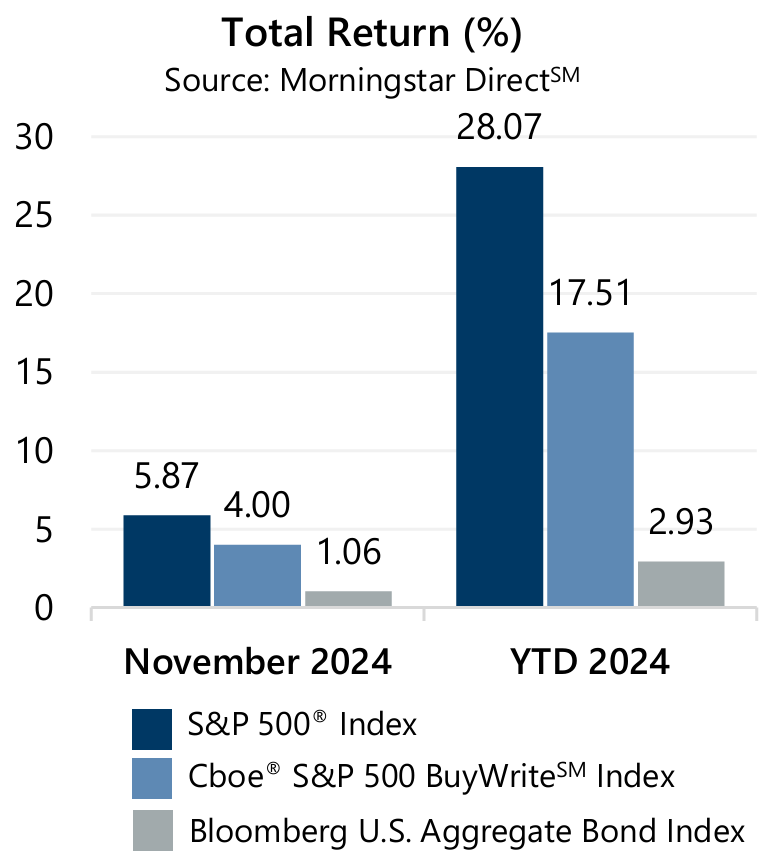

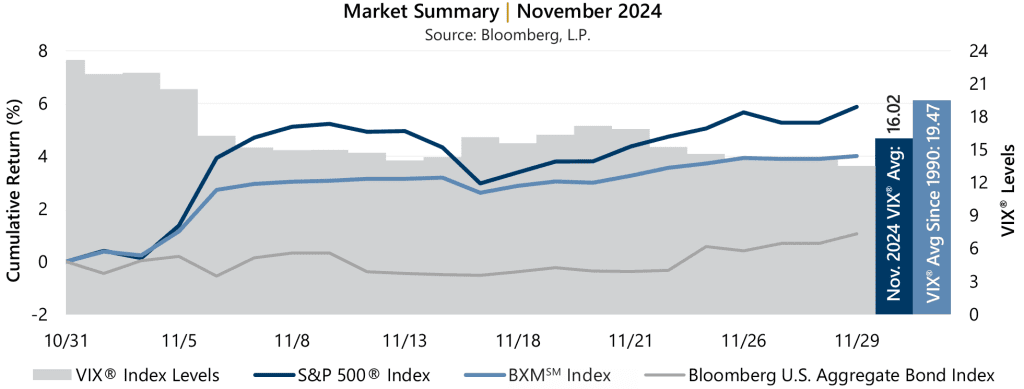

Investors seemed thankful that election uncertainty had been cleared from the table with the S&P 500® Index climbing 5.87% during November. The equity market climbed 2.53% the day after the U.S. presidential election, its highest daily return since November 2022 and its first daily return of +2% or more since August 2024. November was the equity market’s highest monthly return of 2024 and ranked as the 10th highest monthly return since January 2020. From the start of the month through November 11, the S&P 500® Index jumped 5.22% before a -2.14% decline from November 11 to 15. From November 15 to month-end, the S&P 500® Index advanced 2.82% to a new all-time high.

Investors seemed thankful that election uncertainty had been cleared from the table with the S&P 500® Index climbing 5.87% during November. The equity market climbed 2.53% the day after the U.S. presidential election, its highest daily return since November 2022 and its first daily return of +2% or more since August 2024. November was the equity market’s highest monthly return of 2024 and ranked as the 10th highest monthly return since January 2020. From the start of the month through November 11, the S&P 500® Index jumped 5.22% before a -2.14% decline from November 11 to 15. From November 15 to month-end, the S&P 500® Index advanced 2.82% to a new all-time high.

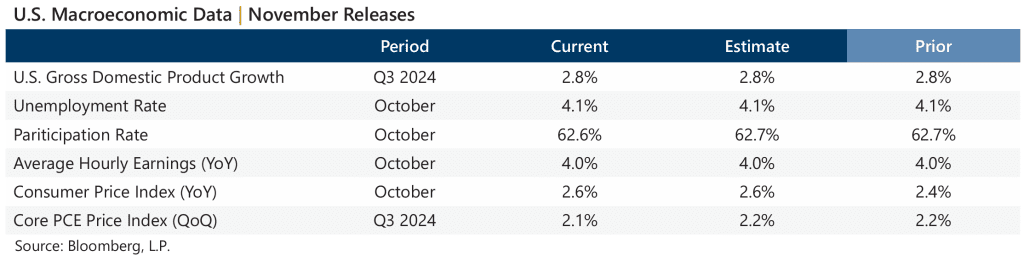

Data released in November revealed an economy that is seemingly in a holding pattern, with a slight uptick in inflation and stable labor market. The second estimate of Gross Domestic Product for the third quarter of 2024 matched the consensus estimates and the prior figure. The year-over-year October Consumer Price Index released November 13, matched consensus estimates but was higher than the prior. The quarter-over-quarter Personal Consumption Expenditures (PCE) Price Index ticked lower than the prior period and the consensus estimates. Corporate earnings were positive in the third quarter with aggregate operating earnings on track to climb 3.3% quarter-over-quarter and 7.8% year-over-year. With more than 96% of S&P 500® Index companies reporting, over 79% have met or exceeded analyst estimates.

The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned 4.00% in November, bringing its year-to-date return to 17.51%. The premiums the BXMSM collected as a percentage of its underlying value provided loss mitigation and are an important component of performance. During the market’s advance from the start of the month to November 11, the BXMSM returned 3.07% compared to the S&P 500® Index’s return of 5.22%. The passive approach of the BXMSM resulted in reduced market exposure as the market advanced, which proved beneficial during the brief decline during the month. From November 11 to November 15, the BXMSM offset 169 basis points of the -2.14% decline in the S&P 500® Index with a return of -0.45%. The BXMSM wrote its new index call option with a December expiration on November 15 and collected a premium of 1.75%. From November 15 to month-end, the BXMSM returned 1.36% compared to the S&P 500® Index’s return of 2.82%.

The Cboe® S&P 500 BuyWriteSM Index1 (the BXMSM) returned 4.00% in November, bringing its year-to-date return to 17.51%. The premiums the BXMSM collected as a percentage of its underlying value provided loss mitigation and are an important component of performance. During the market’s advance from the start of the month to November 11, the BXMSM returned 3.07% compared to the S&P 500® Index’s return of 5.22%. The passive approach of the BXMSM resulted in reduced market exposure as the market advanced, which proved beneficial during the brief decline during the month. From November 11 to November 15, the BXMSM offset 169 basis points of the -2.14% decline in the S&P 500® Index with a return of -0.45%. The BXMSM wrote its new index call option with a December expiration on November 15 and collected a premium of 1.75%. From November 15 to month-end, the BXMSM returned 1.36% compared to the S&P 500® Index’s return of 2.82%.

The Bloomberg U.S. Aggregate Bond Index returned 1.06% in November, bringing its year-to-date return to 2.93%. The yield on the 10-year U.S. Treasury Note (the 10-year) ended October at 4.28% and reached its intra-month high of 4.45% on November 13, before falling to close the month at an intra-month low of 4.17%. The yield curve remained inverted with rates on maturities of 12-months or less exceeding that of the 10-year at the end of November.